GRAB: Platform power in an emerging digital economy

By TickerTango

Introduction

Grab is a leading Southeast Asian technology platform with ambitions to become a dominant super app, offering services across ride-hailing, food delivery and financial services. While it already holds a strong market position in mobility and delivery, the company continues to diversify and expand, particularly in fintech. Grab benefits from favorable economic and demographic tailwinds, yet faces intense competition and skepticism from public markets following its SPAC-led listing.

In a region defined by rapid growth and digital adoption, the company stands at the intersection of opportunity and risk. This thesis explores whether Grab can turn its early lead into a lasting advantage and what that might mean for investors betting on Southeast Asia’s digital future.

History

With prize money, personal savings, and an investment from his mother, Anthony Tan and his co-founder Hooi Ling launched MyTeksi in June 2012, establishing headquarters in Kuala Lumpur. At the time, Malaysia’s taxi service was infamous for being unreliable, unsafe, and widely considered one of the worst in the world. Many passengers faced long waits, refusal of rides, and concerns over personal safety. Motivated to solve these problems, the founders created a mobile app that connected passengers with trustworthy taxi drivers, improving convenience and security. Anthony’s choice to build his own venture instead of joining the family business caused a deep rift and even led to his father disowning him. Despite this personal setback, he was driven by a determination to prove himself and build a successful company.

In 2016, MyTeksi received an investment from Temasek Holdings, which enabled the company to relocate to Singapore and rebrand as Grab. The move marked a pivotal step its evolution from a local taxi app to a regional technology powerhouse.

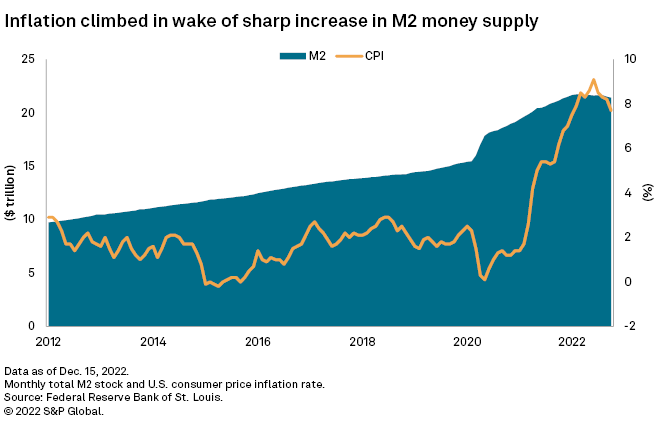

Like many companies that went public via Special Purpose Acquisition Companies (SPACs) around 2020, Grab faced a rocky market debut. SPAC mergers are quicker and less scrutinized than traditional IPOs, making them attractive during the COVID-19 pandemic, which saw a massive increase in money supply (fun fact: 40% of all U.S. dollars in existence were printed between 2020 and 2022). This liquidity surge led to inflated valuations, particularly for growth stocks like Grab, resulting in significant post-listing losses for retail investors.

Business segments

Grab's business model consists of three primary segments:

Delivery

This segment includes GrabFood, a leading on-demand food delivery service, and GrabExpress, which offers parcel and package delivery. GrabFood dominates key markets like Indonesia and Vietnam, while GrabExpress supports e-commerce logistics.

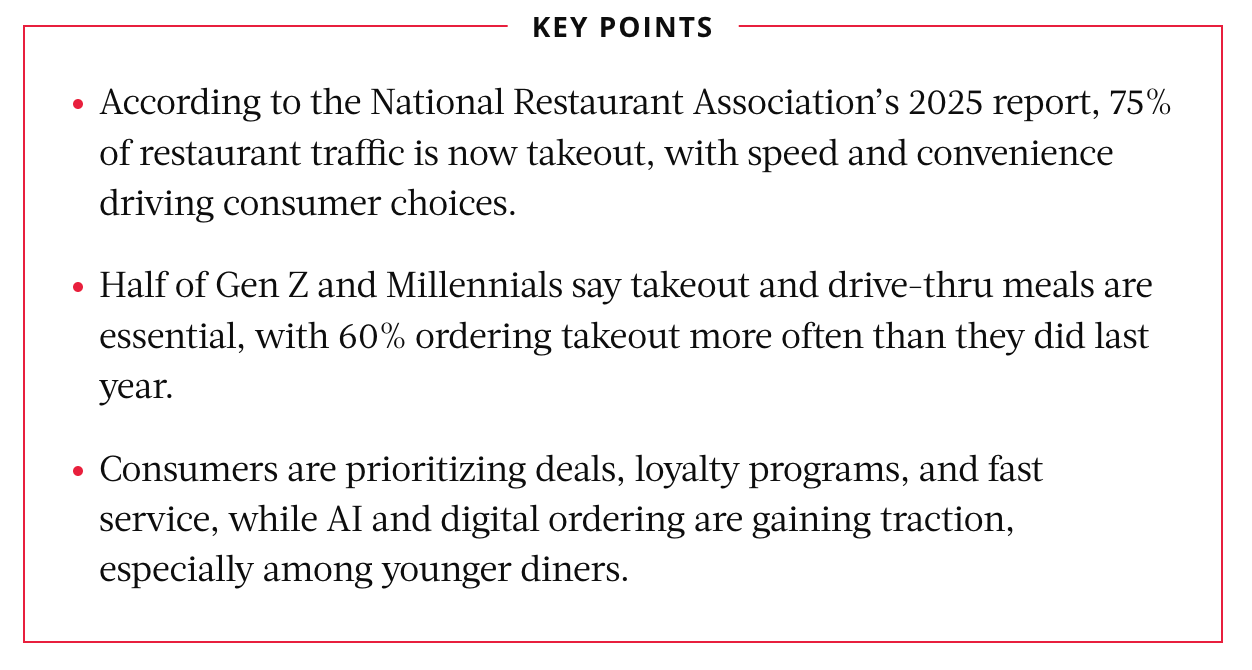

Consumer behavior is shifting fast. According to the National Restaurant Association’s 2025 report, 75% of all restaurant traffic in the U.S. is now takeout, driven by speed and convenience. Half of Gen Z and Millennials consider takeout and drive-thru meals essential, with 60% ordering takeout more frequently than last year. They increasingly prioritize deals, loyalty programs, and seamless digital ordering, especially via AI-enhanced platforms. Takeout is no longer an occasional treat, it’s become a core part of everyday life. I see the same cultural shift gaining momentum in Southeast Asia, and Grab is well-positioned to ride that wave.

Mobility

Grab’s ride-hailing services cover cars, motorcycles, and taxis, holding strong market leadership in Southeast Asia with approximately 50% market share in Indonesia and around 60% in Vietnam. Despite growing competition, Grab innovates in mobility with AI-powered route optimization, electric vehicle pilots, and real-time safety monitoring. This segment remains the backbone of Grab’s ecosystem, driving frequent user engagement and serving as a gateway to cross-sell other services like food delivery and financial products.

The mobility service is especially popular among tourists, who appreciate being able to travel across Southeast Asia using a single app without the hassle of switching between local providers. It’s equally convenient for Southeast Asians traveling within their own countries.

Financial services:

The fintech arm includes GrabPay (a digital wallet for seamless payments), GrabInsure (insurance products), and lending services like microloans for users and small businesses.

Grab is also reaching the underbanked and underserved through its digital banks, GXS Bank (Singapore) and GXBank (Malaysia). Customer deposits in its digital banking business surged to $1,432 million in Q1 2025, up from $479 million in Q1 2024 and from $1,225 million in Q4 2024. Over 90% of GXBank’s customers are Grab users, strengthening the ecosystem’s synergy. GrabFinance specifically targets the unbanked population.

This part of the business is perhaps what I’m most bullish on. Looking at the rapid growth of financial services for companies like MercadoLibre (MELI) in Latin America and Sea Limited (SE) in Southeast Asia, it’s clear this segment is a major driver. Both companies generate a significant part of their revenues (as primary e-commerce players) from financial services, underscoring the enormous potential in this space.

For context:

MELI Q1 2025 total fintech net revenue: $2,632 million

SE Q1 2025 total fintech gross revenue: $787 million

GRAB Q1 2025 total fintech gross revenue: $75 million

Sea Limited’s Monee is clearly ahead, but with 45 million monthly transacting users, Grab’s fintech business has the foundation to scale quickly. More than 60% of Southeast Asia’s population (680 million people) remain unbanked or underserved, highlighting the huge potential for boosting financial inclusion. In comparison, only around 20% of Latin America’s 670 million people are underbanked. This shows just how much runway remains for both Grab and Sea Limited. As digital infrastructure, smartphone penetration, and regulatory support continue to improve, there’s substantial room to scale financial services.

Economic & Demographic tailwinds

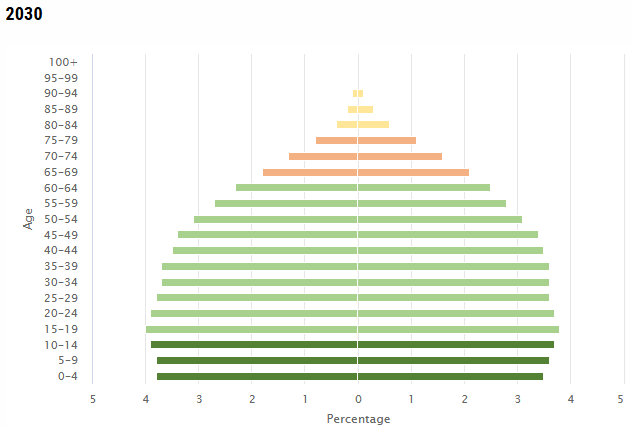

Beyond the structural gaps in financial access, Southeast Asia also benefits from favorable macro trends. One of the reasons I recently turned Grab into a core portfolio holding is the favorable demographics of Southeast Asia. The region’s young and growing population (average age between 30-35) is tech-savvy and increasingly adopting digital solutions.

Source: https://www.population-trends-asiapacific.org/data/sea

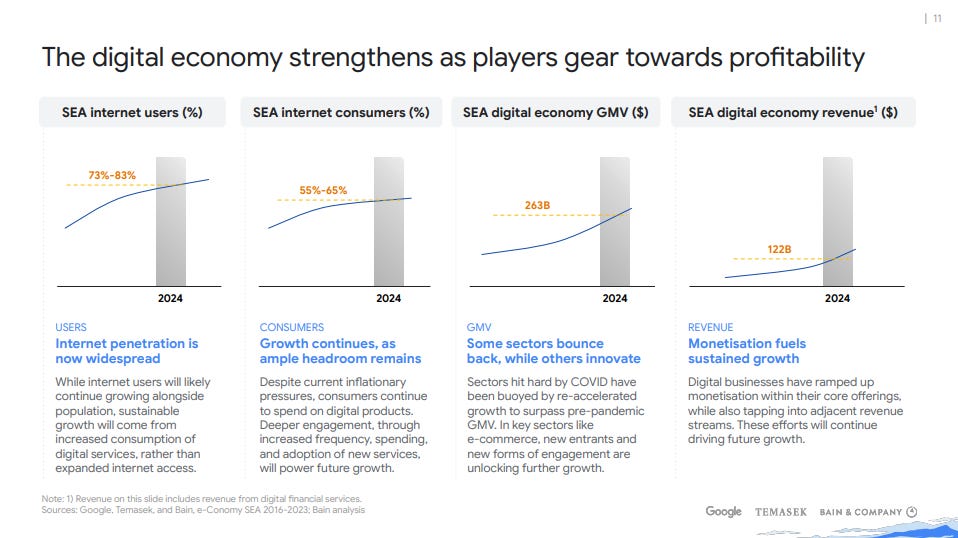

Internet penetration has risen significantly, with 80 million new users coming online between 2020 and 2021, bringing the overall penetration to 75%. However, the digital economy accounts for just 7% of GDP, compared to 35% in the US and 16% in China, indicating ample room for growth.

Southeast Asia’s digital economy demonstrated strong performance in 2024, achieving double-digit year-on-year growth across key metrics. The region's Gross Merchandise Value (GMV) reached $263 billion, a 15% increase, while revenue grew to $89 billion (+14%) and profit rose to $11 billion (+24%). Digital financial services expanded by 22%, driven by the adoption of QR code payments and increased use of digital lending.

Source: https://economysea.withgoogle.com/report/

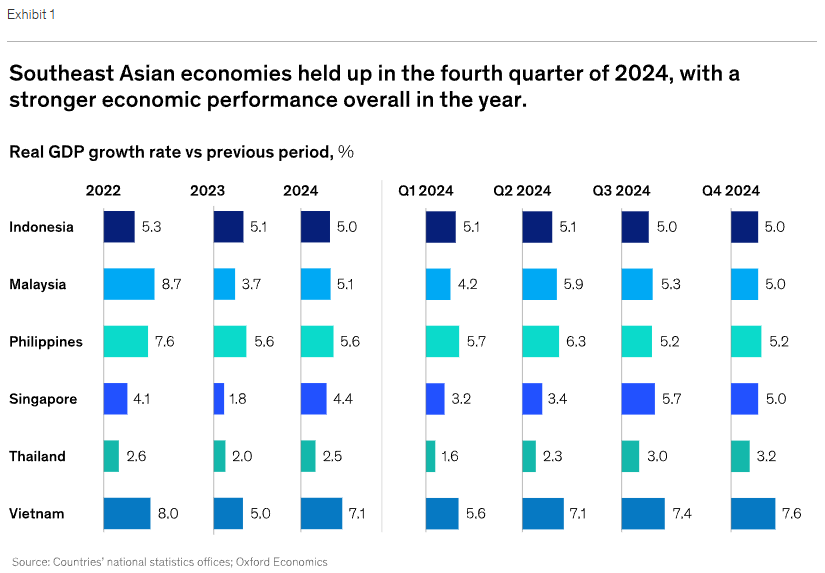

The region's economic resilience was also evident, with most Southeast Asian economies growing by at least 5% in the fourth quarter of 2024, and Vietnam outperforming at 7.55%. This robust growth, supported by a young, productive population and increasing digital adoption, highlights Southeast Asia’s substantial potential for continued expansion, even amid global uncertainties.

Source: https://www.mckinsey.com/featured-insights/future-of-asia/southeast-asia-quarterly-economic-review

Moat

Grab’s integration into daily life in Southeast Asia is profound, so much so that “to grab” has become a verb in everyday conversation, much like how “to Google” means to search online. This linguistic integration signifies strong brand dominance. Grab also benefits from powerful network effects: as more users join the platform, more service providers (drivers, restaurants) are attracted, which in turn draws even more users. The company’s large scale and intangible assets, such as data and brand loyalty, further cement its competitive moat. As of Q1 2025, Grab’s ecosystem includes over 9 million drivers and merchants across eight countries, creating a self-reinforcing cycle that competitors struggle to replicate.

Competition landscape

The competition within the ride-hailing and food delivery sectors is intense. The dominant business model focuses on capturing market share through aggressive incentives, often at the expense of profitability. This practice has resulted in many companies operating at a loss, with smaller competitors frequently being acquired or pushed out. This trend is not unique to Southeast Asia; in Western markets, companies like Delivery Hero, Prosus, and Just Eat Takeaway have similarly pursued consolidation strategies to dominate the market. The outcome is the gradual emergence of large, entrenched players, making it increasingly difficult for smaller, new entrants to compete.

Grab’s acquisition of Uber’s Southeast Asian operations in 2018 marked a key step in consolidating its market position, reflecting a broader strategy of eliminating competition through acquisitions. As part of the deal, Uber initially received a 27.5% stake in Grab, although this percentage has since decreased due to share dilution and sales of Grab shares by Uber. To me, Uber’s decision to exit the Southeast Asian market is a testament to the execution of Grab’s management team. In Southeast Asia, many of Grab’s competitors including Easy Taxi, Uber (in the region), and Ojek, have been outcompeted or acquired, leaving the ride-hailing market increasingly dominated by a few major players. Grab’s main rival, Gojek (GoTO), remains one of the few significant challengers, though ongoing merger talks have faced regulatory obstacles. If a merger were to occur, the combined entity could control around 90% of the market in key regions like Indonesia and Singapore. Such consolidation would undoubtedly benefit margins, as reduced competition typically allows for more pricing power and operational efficiencies.

To me, there is smoke where there is fire, as many signs point to the merger being actively pursued. At the end of last month, Steven Tishman joined Grab’s Board of Directors, bringing extensive M&A experience. In addition, Grab reportedly initiated talks to secure a bridge loan of up to two billion dollars to support the potential acquisition of GoTo. While management teams have declined to comment and Singapore’s competition watchdog has yet to receive formal notification, these developments suggest Grab is seriously preparing for the acquisition.

Valuation & Institutional ownership

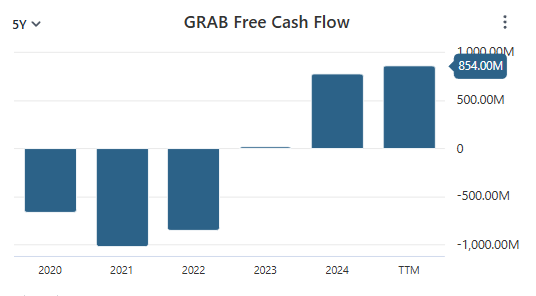

Grab’s financials show a solid upward trend. In Q1 2025, trailing 12-month free cash flow rose to $157 million, driven by operational efficiencies and disciplined cost control. Adjusted EBITDA hit a record $106 million, up 71% year-over-year, supported by growth in on-demand GMV and revenue.

Commenting on the results, CFO Peter Oey noted that the company achieved another quarter of record revenues and expects continued momentum in GMV and revenue growth. Reflecting this confidence, Grab raised its full-year adjusted EBITDA guidance to $460–$480 million.

A guidance raise for the full year is noteworthy amidst political tensions and uncertainty around tariffs, reflecting management’s confidence in sustained growth and strategic execution.

One potential risk to monitor is the growth of partner incentives relative to revenue. In Q1 2025, incentives increased by 22%, outpacing the 18% rise in revenue. If this trend continues unchecked, it could pressure profitability. That said, I’m not overly concerned at this stage. Like Uber in its early days, Grab is using incentives as a strategic tool to capture market share. During the pandemic, Uber flooded users with discount vouchers; now they’re rare. This pattern reflects a common approach: aggressively investing in incentives early on, then scaling them back once market dominance is achieved, thereby improving margins.

Grab’s market capitalization is approximately $20 billion, with cash reserves of $5.9 billion (net cash of $5.55 billion after $350 million in debt), meaning roughly 30% of its market cap is cash. The enterprise value (EV) is $14.45 billion, and with TTM revenue of $2.80 billion, the EV/sales ratio is 5.16, indicating a reasonable valuation for a high-growth tech company with substantial cash backing.

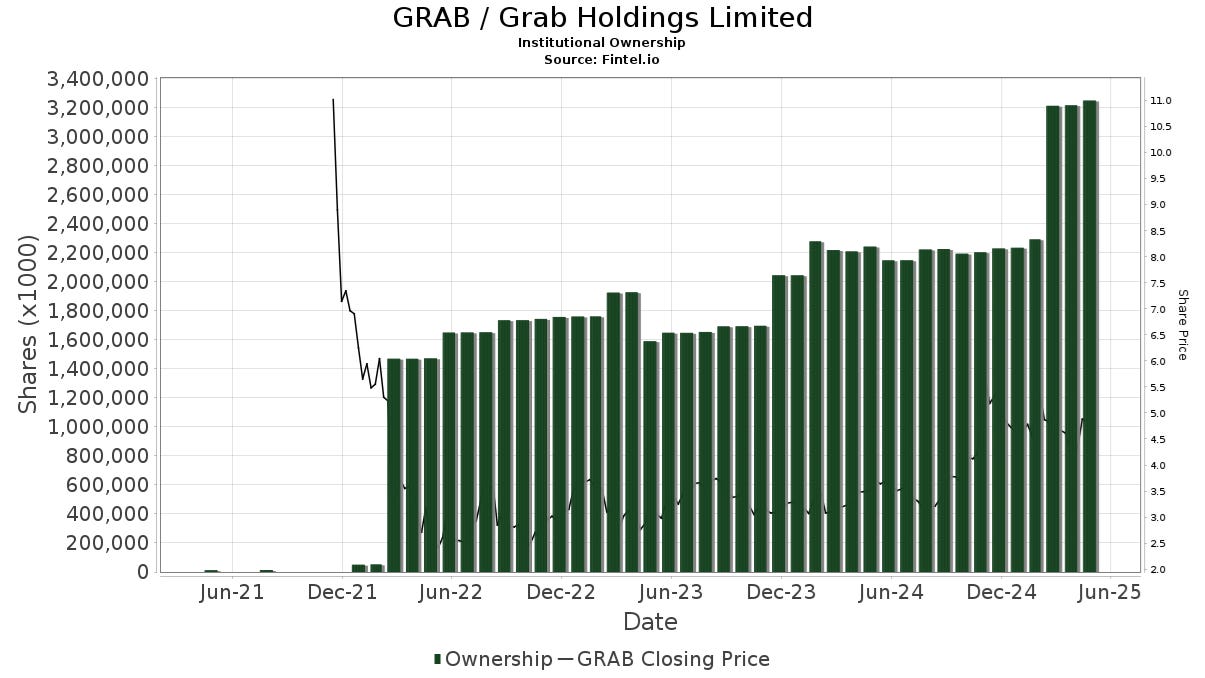

Institutional investors also seem positive about Grab’s future, currently holding nearly 83% of the company’s shares, a clear sign of confidence in its business model and long-term growth potential. As interest grows, ownership could rise to around 90%, leaving new shareholders to compete for the scarce remaining shares (assuming institutions don’t sell, of course).

Interestingly, the Q1 2025 13F disclosures reveal how many shares some of the major players have recently added to their portfolios, with several noteworthy moves:

Howard Marks of Oaktree Capital Management established a new position in Grab by acquiring 10,275,955 shares.

Ray Dalio of Bridgewater Associates increased his position in Grab by 329%, adding 5,097,365 shares.

UBS Asset Management significantly increased its Grab position by 18.37%, adding 2,679,277 shares.

I’m not a technical analysis (TA) type, but it’s worth noting that Grab’s stock has been consolidating for four years now. In my view, a breakout is only a matter of time. As the saying goes: “the bigger the base, the bigger the rip”.

Source: Zastocks

Bear case:

Despite its strong market position and long-term potential, Grab faces several near-term headwinds that could limit upside:

FX pressure

A strengthening US dollar, as measured by the DXY index, poses a significant headwind for Grab due to its operations in Southeast Asia, where local currencies are sensitive to dollar fluctuations. An appreciation of the DXY tends to weaken these currencies, reducing the dollar-denominated value of Grab’s revenue, which is primarily earned in local currencies.

High incentives relative to GMV

Grab continues to rely heavily on customer and driver incentives to drive growth in gross merchandise value. Incentives accounted for 12% of GMV in Q1 2025, slightly down from 13% in 2024, but still significantly higher than mature peers like Uber, where incentives represent about 5% of GMV. These elevated incentives compress margins and delay the path to full profitability.

Growing competitive pressure:

Grab faces escalating competition across Southeast Asia’s digital economy. In Indonesia, GoTo holds around 40% of the ride-hailing and food delivery market, just behind Grab’s roughly 50%, and competes with its own superapp approach. In Vietnam, Xanh SM’s low prices are squeezing Grab’s margins. Meanwhile, e-commerce giants Shopee and Lazada are pushing hard into delivery, putting further pressure on Grab’s superapp growth. Regulatory hurdles could block a Grab/GoTo merger, limiting market consolidation. These headwinds may cause user losses, push promotional costs (incentives) higher, and hold back margin growth.

Conclusion

I often think about this quote by Antonio Linares: “To make life-changing investments, you need to get good at spotting businesses that are on the verge of rapidly increasing their FCF per share, before the market catches up. We live in a world shaped by networks, where real value often shows up on the income statement much later. You need a deep understanding of how value is built inside these networks. In networks, scale takes priority over profits in the early stages. Once you build the largest network, you can turn your focus to making money”. Grab fits this model well, making it an interesting opportunity for patient investors who understand network business dynamics.

Grab has the potential to become Southeast Asia's dominant super app. It is already the market leader in ride-hailing and food delivery, and its fintech arm is rapidly expanding with digital payments and lending. The app’s ecosystem encourages user retention through a flywheel effect: the more services users adopt, the more likely they are to stay within the platform. According to CEO Anthony Tan, only 6% of Southeast Asia’s population currently uses the Grab app on a monthly basis, leaving 94% as untapped potential. I find the stock reasonably valued given this growth runway and I have confidence in the management’s ability to execute on their vision.

Disclaimer: The information presented herein is for informational purposes only and does not constitute financial advice.

If you enjoy updates and write-ups about tech stocks like this one, feel free to follow me on Twitter: TickerTango